As tensions escalate between the U.S., Israel, and Iran, the Islamic Revolutionary Guard Corps (IRGC) has blocked the Strait of Hormuz, prompting South Korea and other major oil importers to seek alternative sources for Middle Eastern crude. Industry experts believe there’s enough supply secured for the next 5-7 years to avoid immediate disruptions, but attention is turning to oil-producing nations farther from Iran.

Industry Ministry Says Limited Market Impact from Crude Futures… Jitters Persist

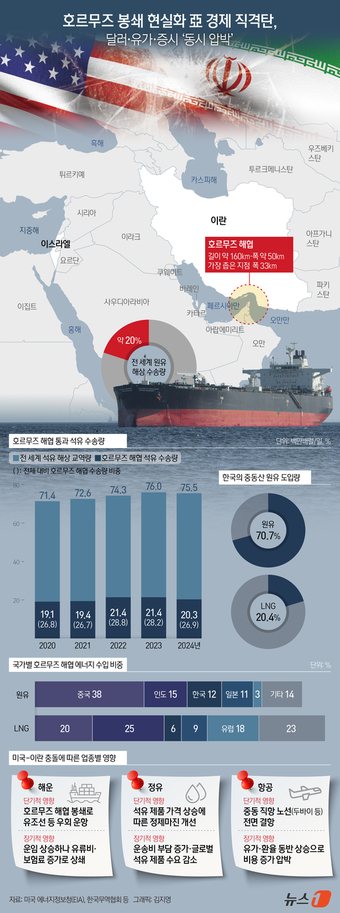

According to the Ministry of Trade, Industry and Energy and industry insiders, about 60-70% of South Korea’s crude oil imports come from Middle Eastern countries like Saudi Arabia, the United Arab Emirates (UAE), and Kuwait. A prolonged blockade of the Strait of Hormuz would inevitably lead to logistics delays and increased shipping costs.

However, the Ministry and refineries typically secure supplies through long-term contracts, reducing the risk of immediate physical shortages. The Korea International Trade Association reports that South Korea depends on the Middle East for 70.7% of its crude oil and 20.4% of its liquefied natural gas (LNG).

A high-ranking official from the Ministry stated that while about 60% of our supply comes from the Middle East, particularly near the Strait of Hormuz, it’s not as concentrated as before. Despite rising crude oil futures prices, the substantial long-term contracts buffer immediate market impacts. If necessary, it can source oil from alternative locations.

On Tuesday, the government convened the Third Real Economy Assessment Meeting to comprehensively review the situation’s impact on resource and energy supply, trade, finance, and various industries. They’ve elevated their response system from director-level to vice-ministerial headquarters. If the crisis persists and private reserves drop below a certain threshold, they’re considering an immediate release of national strategic oil reserves.

Potential alternatives include blending U.S. and Venezuelan oil, both geographically distant from the Middle East. The U.S., now a net exporter post-shale revolution, can ship to Asia via the Gulf of Mexico without passing through the Strait. There’s precedent: last year, the Korea National Oil Corporation swapped 6 million barrels of Middle Eastern heavy oil for U.S. light oil during a strategic reserve adjustment.

Venezuelan oil is another option. With the world’s largest confirmed oil reserves, Venezuela’s heavy and extra-heavy crude could be blended with U.S. light oil to meet some refinery specifications, according to analysts.

Norwegian North Sea crude is also considered a viable alternative for some refineries. However, differences in oil characteristics may affect refining yields, necessitating technical adjustments for full substitution. Transportation costs to South Korea remain a factor.

Within the Middle East, some oil flow could be maintained if infrastructure like Saudi Arabia’s east-west pipeline and the UAE’s Abu Dhabi-Fujairah pipeline becomes operational, bypassing the Strait.

The main concern is oil availability. Countries might restrict exports citing energy security. Geopolitical risk analysts at SpecialEurasia note that Saudi Arabia and the UAE’s combined daily output of 8.5 million barrels falls short of replacing the current 20 million barrel daily flow through the Strait.

Historically, when actual supply disruptions haven’t occurred, price volatility has been the primary shock. The 2019 attack on Saudi Arabia’s Abqaiq facility saw oil prices surge over 10% in a day, taking weeks to stabilize. Following Russia’s invasion of Ukraine in 2022, the International Energy Agency coordinated a strategic reserve release among member countries to temper price increases.

The government is implementing a response strategy combining domestic strategic reserves with the International Energy Agency’s (IEA) cooperative framework. On Tuesday, Deputy Minister Lee Ho-hyeon held a video conference with IEA Executive Director Fatih Birol to assess the Middle Eastern situation’s impact on global energy markets.

Extended Turbulence Lasting Weeks Raises Risk of a Surge in Oil Prices

The key variables are the blockade’s duration and intensity. A short-term threat could be managed through supply diversification and strategic reserves. However, if a substantial blockade lasts for weeks, analysts warn that rising freight and insurance costs could push oil prices above 100 USD per barrel. Professor Heo Yoon from Sogang University’s Graduate School of International Studies emphasized that the Strait of Hormuz blockade could be prolonged, necessitating an emergency plan to proactively increase alternative crude imports from the U.S. and elsewhere.

Conversely, some experts believe a quick resolution could reduce uncertainty. Choi Jin-young, an analyst at Daishin Securities, noted that while a Hormuz blockade is serious, alternative routes like the Cape of Good Hope could mitigate disruptions, similar to past Israel-Hamas conflicts. Though immediate price volatility is expected, uncertainty should subside within three months.

{kind=link}